You hear it on the radio all the time – the 40 year old male that could get a 20 year $500,000 term life insurance policy for only $30.62 per month. The inference from this statement is that if you are a 40 year old male – that you could get a $500,000 life insurance policy for that price too.

Sorry to tell you that this assumption – may be totally wrong. In fact its so wrong, I honestly found these advertisements to be more harmful than helpful.

In this short article we are going to go through point by point why these general term life insurance quotes might be bogus and probably won’t apply to you.

Life Insurance Quotes: Height / Weight

Doesn’t it feel weird listening to ads listing people’s height and weight? Oh wait – term life ads almost never bring up height and weight. That is pretty funny because as an insurance agent, who specializes in term life insurance, I can tell you that the height weight matrix is the first stop in the insurance quoting process. I do not give anyone any quote without first consulting these charts. Insurers live by these charts. Agents pin them on the wall. They are by and large the quickest and easiest one item to start with.

Generally speaking the heavier you are for your height; the more life insurance will cost you. So how do these quotes generate their pricing? Simple – They just assume you are super trim. That is largely problematic though. According to the CDC (in 2014), about 70% of Americans 20 and over are overweight in some form or another. 70%! Admittedly it is a bit difficult to level out what the CDC believes is overweight while pairing this with hundreds of insurers different build charts. However you can see the obvious issue with just assuming anyone is the so called ideal weight. In short if you weight more – you will pay more.

The Rest of your Health:

There are lots of other factors besides your height and weight that determine how much for life insurance you will pay as well. Let us not let that same CDC report get away from us, as there is lots of other useful information on it.

Percentage of Americans that have Diabetes: About 12%.

Percentage of Americans that have Hypercholesterolemia: 27%.

Percentage of Americans that have Hypertension: 31%.

Any three of these conditions can knock you out of best in class pricing, any of them and many many more. People that have other major issues such as Asthma, Sleep Apnea, Cancers, COPD, Liver Issues, etc – all of them are subject to increased rates from life insurance carriers. People that have had major operations or that take basic prescriptions too will often miss out on best in class rates.

In fact many carriers also look at the health of your direct relatives such as your parents. Have your parents been diagnosed with cancer before a certain age? So how do the life insurance ads accommodate for health in proposing insurance rates? Typically they assume that you are in perfect health and have never had a major health issue nor take any prescription.

What you Do:

Insurance companies don’t just focus on your health and weight though – they will also want to know about your career. There are many careers where it is rather obvious what the risk is, such as roofers. Others, such as truck drivers, loggers, construction worker, etc. may not seem so clear. However all of these people too, just based off of what they do for a living are not likely to get that best in class rate, at least with some carriers. It’s statistically difficult to estimate how many Americans work in these roles, but we can guess that is around 20%.

As one can quickly see there is a pile of roadblocks for everyone to qualify for “best in class” term life insurance pricing.

State Specific Issues:

State specific life insurance rates are not what they once were, however not all life insurers offer all rates or even coverage in all states. Almost all insurance in the US is regulated by the individual states, which means that a given life insurer has to contend with more than 50 different regulatory bodies when you take into account overseas territories. That is a ton of red tape. This is just another example of how a promoted rate may not be your solution.

Foreign Travel and Citizenship:

Another non spoken requirement to even acquire life insurance is that you must be some form of a “resident” of the United States. Insurers differ on this, but most carriers will not allow you best in class insurance prices if you travel a lot. Most insurers will not even issue any sort of policy to you if your travel is extensive or if you have gone to (or plan to in some cases) certain countries determined by the State Department to be considered dangerous.

So what Do the Life Insurance Ads Really Tell You?

As we have shown you there are several major factors that can increase anyone’s life insurance pricing (and we have not even gone through all of them.) There are also numerous considerations that would even block you from getting any type of life insurance. As with any form of advertisement that promises a product “could cost you something” that does not mean it actually will. All these ads are really demonstrating to you is that someone in perfect health, in a safe job, who weighs the right amount, and never travels – may be able to get insurance at that price.

What the Rest of Us Can do:

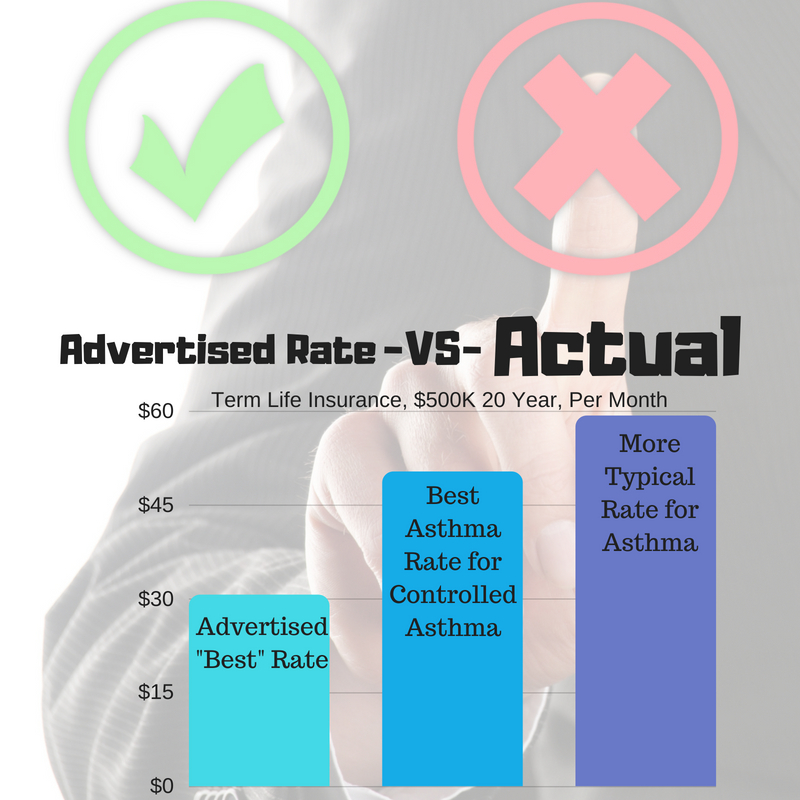

For the rest of us (I have asthma) this just means that we need to shop around and find the best product for your specific situation. Taking asthma a classic example, as it is somewhat prevalent in the American population (7.6%)- the cost for what you will pay for term life insurance with asthma will depend on your exact health status AND the insurer you work with. This is where finding a solid agent can help you considerably. Some insurers may only offer a certain client with controlled asthma standard nonsmoker, while others ‘may’ be willing to offer you preferred nonsmoker pricing. These two prices are vastly different. When compared with the quoted price difference from some generic ad it so far off as to be almost amusing.

An Example of Life Insurance Premium Price Differences:

Using our 40 year old male from our previous example – we can run the numbers for him assuming he also has some form of asthma. It is controlled and he is under the care and supervision of a doctor and has never been hospitalized due to it. He takes medications daily and refills his prescriptions on time regularly. He qualifies for the best height weight, has no other health issues, his parents are alive and in perfect health, and he has a boring safe job as an accountant. There is nothing else about his situation that would prevent him from securing a $500,000 20 year term life insurance policy.

So how does his pricing look? Remember our advertised rate for a 40 year old male for $500,000 in term insurance was only $30.62 per month. But many carriers will only offer you a standard nonsmoker rate of $59.25 per month. If you shop the carriers though you may be able to find one that will offer a preferred rate and that rate can save you big bucks at $50.31 per month. Although that $50 month amount may seem like a letdown when compared with the advertised rate, at least it’s a real number.

The Truth About Life Insurance Quotes:

The real story with term quotes is that in order for them to be accurate for you, they must have your true information. All the specifics about you. There really is no way for this to happen without “your information,” and therefore general advertised rates will likely not pertain to you and your family. The real truth is that advertised pricing on most things at best offers up the “lowest possible” price and not the final actual price. Consumers would do best by contacting a trusted and licensed source to ascertain their most accurate quote.

Scott W Johnson is a financial author and insurance agent based in California and is the owner of WholeVsTermLifeInsurance.com.