There is blood in the streets, as the saying goes. Figuratively and, in light of recent news, all too literally. With COVID 19 hysteria, among other things, sending the stock market into a free fall, long-term investors are reminded that the bull market couldn’t last forever. Newer investors are getting their first taste of real volatility and having their risk tolerance assumptions tested with real stakes. Depending on how close you are to retirement and how diversified your stock portfolio is, when the stock market becomes erratic it can be hard to know whether to cut your losses. So, what should you do when stocks start plummeting?

Well, you always have three options: buy, sell or do nothing, but for the long-term, well-diversified investor, buying is the only move that makes sense. If you’re like me, invested mostly in index funds that track the entire US or world markets, all you need to profit is time. Enough, at least, for a recovery when the markets crash. Though an individual stock can lose 100% of its value, the only way that a broadly diversified index fund can fold is if every company in the index does. If that happens you have bigger problems anyways, like post-apocalyptic survival. For funds that track the total US Market, a complete loss of value is a virtual impossibility. I’m betting everything that it is anyways.

Whether you dollar cost average the traditional way – buy at specified times regardless of market movement – or you buy the dip, investing and re balancing over time is the most consistent way to build wealth with stocks. I don’t think I need to go into detail on why selling during a downswing is a bad idea. So what’s wrong with doing nothing?

Do-nothing plans are typically coupled with expert advice that, “we haven’t yet seen the bottom of the market so you should wait to invest.” However, no one knows with certainty where the bottom of the market will be, and timing the market doesn’t works for long.

There’s nothing wrong with making informed investment decisions though. Especially since you can do so without additional risk.

The Problem With Dollar Cost Averaging

Dollar cost averaging attempts to take emotions out of investing to reduce the possibility off a sell-off during negative market movements. Investors are advised to ignore so called “market noise” and invest at the same time every year without even looking at stock prices. This is done with the understanding that the market will increase over time, regardless of the price of shares today. In fact, studies have shown that historically, even if investors only bought in at the top of the market every year, they would have still become millionaires if they stayed the course until retirement.

However, the problem with this type of dollar cost averaging is that it assumes that you are incapable of disciplined investing, that you would otherwise attempt to time the market to your own detriment. It also implies that there is no tangible way to plan investments without additional risk. Thus, traditional dollar cost averaging is typically self-monitoring for investors with asset allocations that don’t match their risk tolerances.

There is a good argument for lump sum investing at the beginning of each year. Even though it’s still arbitrary investing, putting your money to as work early as possible has proven to be an effective strategy for long term investors. For that reason I also strive to invest as early as possible each year, but I still prefer to have a more control of price-per-share when possible.

Buying the Dip Beats Dollar Cost Averaging

The bull market has taken a beating

Even in a bull market there are moments every year when stocks dip briefly yet significantly. Enough, at least, to present investment opportunities. When stock values fall during a bull market it typically takes days to weeks before they rebound, giving you multiple chances to invest. Rather than investing arbitrarily, you can buy additional stock when values fall by a 2%- 5%, for example. You can do this somewhat automatically with stop-loss or stop-limit orders. You don’t have to anticipate the bottom, you just need to react to market fluctuations after they occur.

If market corrections are atypical and stocks don’t regain their previous values quickly (the market crashes), almost no one realizes what’s happening until it’s too late. Therefore, it makes sense to invest in tranches as stocks get progressively cheaper. I recently purchased Vanguard’s US Small Cap Fund, VBR, at $114 dollars per share, then $108, $102 and $91. This is also a method of dollar cost averaging, but this strategy allows you to get the best averaged price-per-share without additional risk. I have no regrets that I didn’t wait for the market to “bottom out.” I received the best average price available in years. Waiting is more likely to keep me from investing at all, due to the fear of missing out on better prices.

As Long as You Keep Investing, You Win Anyways.

This image shows the price of VTSAX during the second leg of a stock market correction. It felt like a great value at the time but the price would be much lower in the days to follow. When that happens it’s easy to beat yourself up for not being more patient. However, this actually was a great time to buy; It was the best price-per-share in a full year. You can always buy additional shares if stocks fall further, but you can’t always lock in your value before the market rebounds.

If we zoom out more we can see that over the last 5 years the US stock market increased in value tremendously despite a major correction (2018) and several minor ones. This begins to illustrate that the longer you’re in the market, the more significantly you are rewarded.

Even with the huge recent drop in price, VTSAX (above) holds the same value as it did after the 2018 stock market had regained much of its previous record-high value.

In this view, reflecting the total US stock market from 2000 to 2020, we can see that the prices secured today are certainly less important than the amount of time once is invested overall. But that doesn’t mean that you shouldn’t aim to plan investments when stocks go on sale. Doing so is likely to significantly increase your nest egg in the long run.

Taking it One Step Further

When there is big news, like for instance a global pandemic or oil negotiations falling apart, or it’s an election year, or all three simultaneously, the market is negatively impacted. Again, this is not the same as market timing the way it is usually attempted. You’re not pouring over candle stick charts for entry and exit points. You’re simply using major events that are currently driving down prices to make informed decisions.

Do you own mutual funds instead of ETFs? If so, you only see the price you secured after daily trading has concluded. However, you can track the ETF equivalent of a mutual fund to determine a good time to buy. That”s because ETFs trade throughout the day. For instance, VTI is the ETF equivalent of the mutual fund VTSAX (it tracks the same index). If VTI is significantly higher or lower at the end of the day, you can bet that VTSAX will be too.

You can also follow the futures market which trades after hours. The futures market reflects how investors perceive value and though it doesn’t guarantee how the stock market will behave on the next trading day, big swings can certainly telegraph major market movements.

A closely related indicator is the Volitility Index (or VIX), which tracks options investments. The VIX moves up when the market is falling and values above 30 are typically signal large volatility, due to increased uncertainty.

This graph reflects volatility (fear) since 1990. It’s no surprise that the periods of highest volatility correlate to periods where the stock market was crashing.

Adjusting Asset Allocation

Adjusting your asset allocation in reaction to market movements is usually considered sacrilegious for typical index fund investors. I don’t recommend it either, but there is an argument for adjusting your cash allocation when stock values drop. When the stock market is overvalued (or keeps hitting record highs) I hold more cash. During downturns I put this cash to work to reap the benefit of lower prices. Remember, your retirement fund should not double as your emergency fund so you shouldn’t have earmarked these funds for any purpose other than investment.

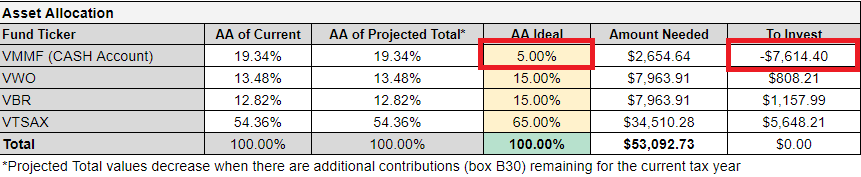

If you have been using the free investment tracking spreadsheet from Valuist – which is a great tool for tracking your average cost-per-share, asset allocation and many other things – you will recognize the image above. By changing my cash position from 10% to 5% I can free up additional funds to invest with.

Final Considerations

As long as your asset allocation matches your risk tolerance and you are invested in well-diversified stocks or funds, your only enemy is time. Instead of arbitrarily dollar cost averaging, use readily available information to make informed investment decisions. A little foresight can make you far wealthier in the long run without unnecessary additional risk. So don’t time the market, react to it.

Do you think that the lump sum method of dollar cost averaging is better than buying the dip?

Useful insights. I tried to share it on FB twice and couldn’t do it.